Another step in the right direction?

When we got our last EPC done in April 2022, we were a little disappointed that there were no recommendations of what to do to reduce our carbon footprint.

Which was the reason behind getting the assessment redone.

As it is, we’ve made some positive steps, hopefully, in the right direction. The lattest one was achieved this week, with the installation of a battery.

What, on top of the V2G?

Absolutely. Don’t get me wrong, the V2G has worked out very well for us, but there’s a couple of things it is lacking.

The first being, we don’t get to say where or when it charges or discharges.

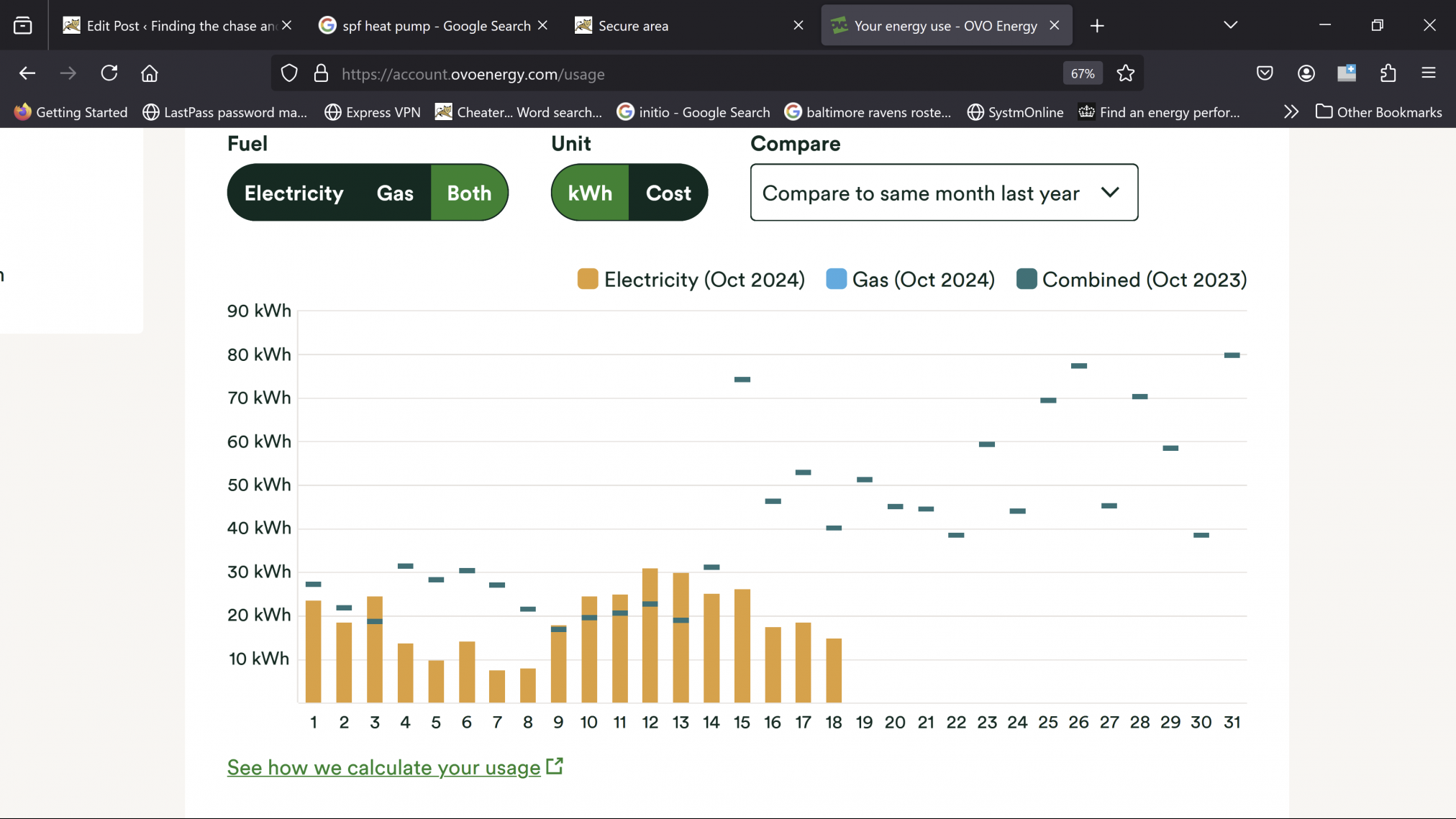

The second being that we want a battery back up for the house. Getting our energy use down means we can, for some of the year, live off the energy we produce from our roof. In summer we often generate more than 15kWh a day and use less than 13kWh. Having access to that power would be really useful.

It’s a little different over the winter as we’re also using electricity to heat our house and water. Being in the UK, we just don’t generate enough power during December and January to be “off grid”.

The idea for our home battery as opposed to using the car battery, is that we can go on “island mode” and disconnect from the grid when we can to or need to, say during a power cut.

There’s other things our system does too. It monitors the power from our solar cells, the power going out to the grid, and the power coming in. During the summer, it can be programme to donate to the grid or our home when prices are highest or when there is a glut of power, store energy for later.

During the summer, we should be able to go off grid for much of the time, effectively. We generate, at most, 3kWh. Our base load, (what the house uses when the heating isn’t running, or lights are on, etc), we use between 0.4 and 0.6kWh – so that excess can go straight into our battery.

Cooking, washing clothes and dishes, and heating are the big consummers in the house. Doing these functions at mid-day can make a huge difference to your electricity bill – even during the winter. Batch cooking can make use of this excess power, so the evening meal needs to be a snack or reheated in the energy efficient microwave.

That takes a great deal of planning and effort. There’s energy consummed by the fridge for keeping things cool, and again that is not a zero cost.

I have mixed feelings about batch cooking for that reason – the more you cook, the more energy you need. Then you waste that energy in cooling it down… There are other options, though again that is more effort.

I’m beginning to think you could go crazy thinking about this!

Posted: November 2nd, 2024 under Driving off the grid.

Comments: none